Flood Maps311Search all NYC.gov websites

Flood Maps311Search all NYC.gov websites

Changes

Flood Insurance Reform

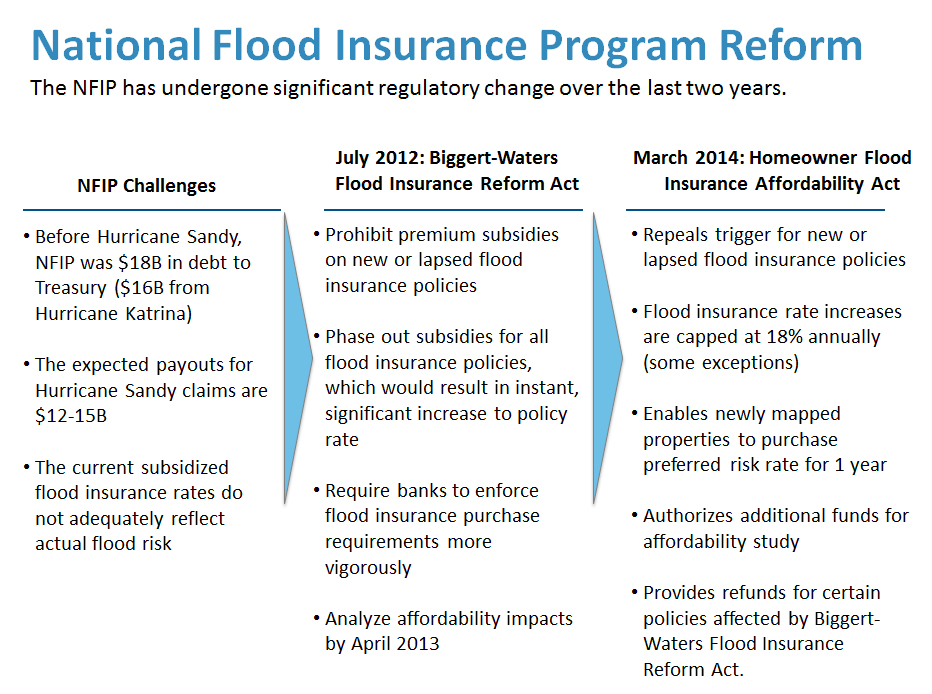

The National Flood Insurance Program (NFIP) was created in 1968 to provide flood insurance for property owners and was made mandatory in 1973. Over time, events like Hurricane Katrina and Rita left the program with over $25 billion in debt. In 2012, Congress passed legislation called the Biggert-Waters Flood Insurance Reform Act (BW-12) to transition the NFIP to a financially sustainable program. The goal of Biggert-Waters was to increase the financial stability of NFIP by decreasing the subsidies on flood insurance policies to more accurately reflect true flood risk.

This means that flood insurance rates increased substantially for flood insurance policies and for homeowners whose properties were are mapped into a high risk zone (find out more about interpreting risk). However, this was a drastic change, and many of the BW-12 price increased were repealed or modified by the Homeowner Flood Insurance Affordability Act (HFIAA) in 2014. While the Homeowner Flood Insurance Affordability Act of 2013 (HFIAA) will mitigate some of the immediate impacts of BW-12, homeowners will see annual increases between 15 and 18 percent as all policies move toward eventually paying FEMA’s newly assessed higher rates. Homeowners could also face lower property values as potential buyers take into account insurance costs.

To better understand the impact that these changes may have on property owners in New York, the City is conducting two **flood insurance affordability studies:** one to access the impact on 1-4 family homes, and another to assess the impacts on mixed-use and multi-family buildings in light of recent flood insurance reforms and the recently expanded floodplain. In addition, to ensure that the public is aware of their flood risk and flood insurance requirements, the City is launching a flood insurance consumer education campaign that will launch this spring.